As a result of provisions in the One Big Beautiful Bill Act (OBBBA) passed in 2025, many medical students will now be paying for a significant part of their education with private student loans. Here is what they need to know.

About 27% of medical students graduate with no educational debt. That means 73% are paying for part or all of the costs of education with borrowed money. For decades, a generous federal student loan program has meant that the only student loans most doctors ever used were federal student loans. Starting in the 2026-2027 year, that will no longer be the case. OBBBA has placed a limit of $50,000 per year ($200,000 total) on federal student loan borrowing. The median total cost of attendance for medical schools ranges from $268,000 (public in-state) to $363,000 (private), as of 2026. That's a median too, so half of the students at each type of school are paying more than that.

For many students, half or even more of their student loans will need to be private loans.

We recommend you check with two or three of these companies and go with the one offering you the lowest interest rate and best terms.

† Bonus may include cash rebates and value of free course. Student loan borrowers who use the WCI links will be enrolled in The White Coat Investor’s flagship course, Fire Your Financial Advisor: STUDENT for free ($99 value). Borrowers may still receive the amazing cash rebates that WCI has negotiated with lenders. Offer valid for loan applications submitted from May 1, 2026 through October 31, 2026. Free course must be claimed within 90 days of first loan disbursement. To claim free course enrollment, visit https://www.whitecoatinvestor.com/loanbonus.

You can do this, and WCI can help! We want you to be successful, so we are giving anyone who secures a loan through WCI Links free access to The White Coat Investor’s Flagship course, Fire Your Financial Advisor: STUDENT (Laying the Foundation for Financial Success). Get amazing cash rebates that we have negotiated AND another $99 in value with the course.

*The course must be claimed within 90 days of loan disbursement. Course access instructions are sent out once a month, generally in the first week of the month.

Get Free Course

The best student loans are the federal student loans. While they will usually offer you a lower interest rate, the real attraction here is the possibility of tax-free forgiveness after just 10 years of payments, via Public Service Loan Forgiveness, for those working full-time in qualifying jobs. In addition, Income Driven Repayment (IDR) programs help keep the payments low during training and even provide the possibility of taxable forgiveness in any job (or no job at all) after 25-30 years of payments for those in desperate situations. Thus, the first $50,000 per year that a medical student needs to borrow for school should be taken from the federal government—your school's financial aid office can assist you with that.

Then what? Then, you need to apply with a private lender, and that's where we can help. Here are the companies we have been working with for years to help doctors refinance their student loans to lower interest rates. That will help minimize costs and get you free of that student loan burden as soon as possible. They also offer the initial student loans that medical students will now need.

As a general rule, we're not big fans of debt. If you have money, at least money outside of retirement accounts, you're generally better off spending that before taking out any student loans, at least private student loans. If your family can assist you, take them up on their offer. Then see the private lenders above for the rest.

Note that the interest clock starts ticking as soon as you take out the loan. So, don't take out loans before you actually need the money. You don't have to borrow an entire year's worth of money in August. You don't even have to borrow an entire semester's worth of living expenses all at once. Naturally, the more loans you take out, the more loans you will have to keep track of, but they can generally all be combined later via consolidation (federal) or refinancing (private).

OBBBA made significant changes to the medical (and dental) school student loan landscape.

Starting with the 2026-2027 school year, a medical student can only borrow $50,000 per year in federal student loans. That number is not indexed to inflation. As the years go by and presumably the cost of medical school attendance continues to rise with inflation, a smaller and smaller percentage of student loans will be federal.

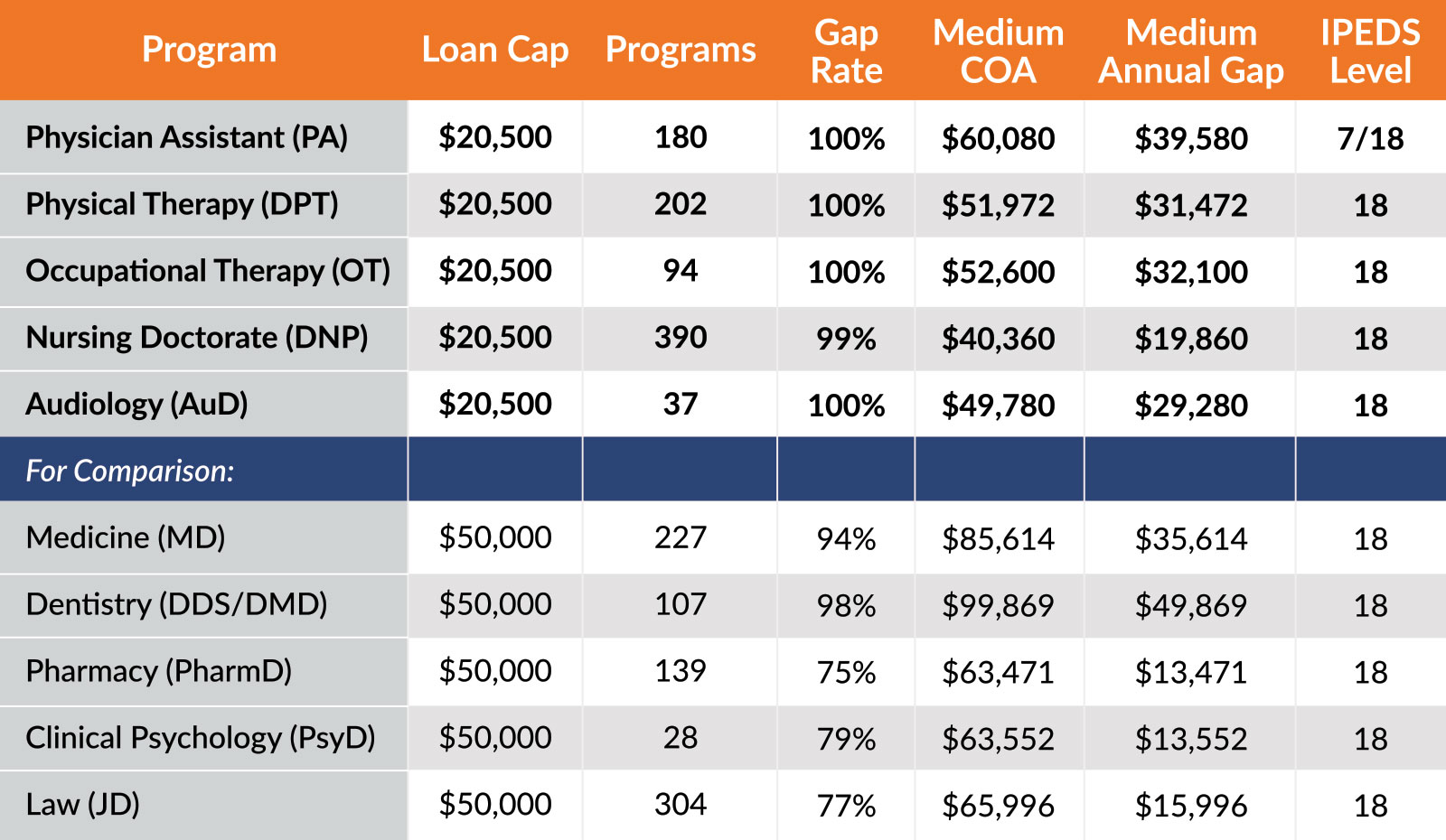

A recent study by the Gap Funding Group found the following:

If you thought it was bad for doctors, consider programs that are classified as “graduate” ($20,000 annual limit) instead of “professional” ($50,000 annual limit).

While that's all very interesting, the bottom line is that many students are going to have a gap, and the only way they can fill it is with private loans. As private loans become more common, the space should become more competitive, and it should become easier to get a “fair” interest rate without a co-signer. Sometimes, private student loans actually have lower interest rates than federal loans. Many WCIers have found they could refinance their loans at dramatically better interest rates with a private lender. The federal government generally never offers a lower rate once a loan is issued, no matter what happens with prevailing interest rates.

Start inquiring with lenders a few months before you enroll in school, as you work out your expected spending for each semester. Use private loans to fill the gap between your expenses and the amount you can take out as a federal loan.

While private lenders will frequently offer both fixed and variable rate student loans, we recommend fixed rate loans until you become an attending and are sure you can afford the worst-case scenario with a variable interest rate. Variable rates are often lower than fixed rates because the borrower is running the interest rate risk. That means more of your payments can go toward principal than interest, allowing you to pay off your loans faster. But there is just too much risk of rates going up for a medical student to take out a variable interest rate loan years before they will begin paying back that loan.

While federal student loans are standardized, every private loan is unique, just like every borrower. As a general rule, however, federal student loans are much more attractive due to their additional features, like the IDR program and PSLF, and protections in the event of death or permanent disability. That doesn't mean that private loans cannot offer more convenience, lower fees, and lower interest rates. However, the general rule while in school should be to borrow the maximum amount of federal loans before taking out any private loans.

As the federal student loan programs became more and more generous, especially with a combination of the now-canceled SAVE IDR program and PSLF, it made sense for a few years for a medical student to borrow as much as they could, since 40% or more of doctors end up in PSLF-qualifying jobs. With the reforms of the OBBBA, however, normality has now mostly returned. That means you should use your own and any family money first and live as frugally as you can during school to minimize the amount of money you borrow, especially via private loans.

Keep in mind that toward the end of school, you will need a little money to do residency interviews, pay moving expenses to a new city for residency, and live on until your first residency paycheck arrives in August after medical school graduation. If you have a little student loan money left over, that might help prevent you from having to take out a high-interest-rate private loan to cover those expenses. Technically, you're only supposed to use student loans to pay for your education. Practically speaking, money is fungible, and nobody is looking (or even cares) if you have a little left over to pay for a U-Haul.

The Repayment Assistance Program (RAP), the newest IDR program, ensures that federal student loans will not grow during residency. That's not the case for private loans, especially if you take advantage of refinancing programs that limit payments to just $100 per month during training. If you are like most doctors, you will owe more at the end of residency than at the beginning.

You can get rid of student loans in two main ways. The first is to get someone else to pay them—usually the taxpayer via the PSLF program, but sometimes a future employer or a state program. The second is to pay them off yourself. Even students using PSLF for their federal loans will usually still need to pay off their private loans themselves. The main method to do so is usually referred to as “Live Like a Resident.” Essentially, your income will increase from something like $70,000 as a resident to something like $250,000-$600,000 as an attending. If you keep living a lifestyle similar to what you lived on with your resident income for 2-5 years as an attending, you can use the difference to quickly wipe out your student loans.

Consider a graduating resident who owes $300,000 in student loans and who will have an income of $350,000 after training. Something like $90,000 will go toward taxes, and if the doc lives on only $100,000, that leaves $160,000 per year that can go toward student loans. That $300,000 student loan debt can then be paid off in about two years.

Federal student loan interest rates are fixed based on a formula that relies on the Treasury bond auction conducted the prior May. For 2025-2026, the rate was 7.94%. General interest rates have fallen since then, so we expect slightly lower rates for 2026-2027.

Private student loan interest rates are far more variable, and they will vary by lender and borrower. It's best to just apply with several of the lenders above to see what rates you will qualify for rather than to guess what your rates will be.

Some student loan borrowers NEVER pay back their student loans. They literally die having never paid for their education. We don't recommend that approach. We think most doctors and similar high-income professionals should either pay off their student loans or have them forgiven within 2-7 years of finishing their training. Combining a reasonable student debt burden with a reasonable income and adding in a bit of financial literacy and discipline, we have found that most white coat investors get rid of their student loans within 1-5 years of finishing training.

Now, a few rapid-fire style questions.

It varies by school and residency, but on average, expect a cost of attendance (tuition and fees plus living expenses) to be in the $50,000-$100,000 per year range. If you multiply that by four years, that is $200,00-$400,000 total.

Grad PLUS loans will no longer be available after July 1, 2026.

Medical school is still a good investment, even if you have to pay for the entire thing with borrowed money. This assumes the following all happens:

Not matching into residency in your chosen specialty can result in a financial catastrophe. You don't get a pass on math. You can't borrow $500,000 in student loans and then plan to work part-time in a low-paying job and expect everything to work out fine. Likewise, it is entirely possible and surprisingly easy for doctors to live paycheck to paycheck, spending their entire income. Data suggests that as many as 40% of high earners ($300,000+) are living hand to mouth. You really do have to live on much less than you earn for a few years to pay off your student loans.

The most common mistake doctors make is treating loan money as Monopoly money. It is a weird thing to have a lender hand you more money than you have made in your entire life. But I assure you that you WILL probably have to pay that money back. So, don't spend any more than you must.

Medical students sometimes take out loans too early. Remember that interest starts as soon as the loans are disbursed, so, to minimize the accumulated interest, don't take out loans until you really need the money. You can always go back to get more, and two weeks is usually plenty of time to have a loan disbursed.

Doctors often fail to have a solid written plan to take care of their student loans. If you need help putting one together, book a consultation with StudentLoanAdvice.com. They'll make sure you're in the right IDR program, that you file your taxes and use retirement accounts properly to improve cash flow and maximize forgiveness, and that you refinance private loans at the right time.

Federal financial aid is generally limited to US citizens and permanent residents. Exceptions exist for refugees, asylees, or those with specific “eligible noncitizen” statuses—such as those holding a green card or certain I-94 classifications.

But typical international students on F-1, F-2, J-1, or J-2 visas don't qualify. They will need to use private loans or personal resources to pay for school. They might, however, be eligible for contract programs such as MD/PhD programs. They are generally ineligible for the Indian Health Service, National Health Service Corps, and the military's Health Professions Scholarship Program.

Starting in 2026-2027, private student loans are now part of the game. We encourage you to visit with our partners below to get the best rates and terms available on private student loans. Then, refinance them early and often whenever you can get a lower interest rate.

Since 2018, Juno has helped graduate students access better student loan options by using the power of group negotiation. Juno was started at Harvard Business School with a simple idea: students should not have to negotiate alone.

We are not a lender. We are a student-first platform that negotiates with lenders on behalf of students to unlock better rates, cash back, and other benefits. This year, we are opening our negotiated medical student loan benefits to eligible medical students.

Through Juno, medical students can:

Our goal is to make student loans more transparent, more competitive, and easier to navigate, so medical students can focus less on financing and more on their training. Options without a cosigner or income, subject to lender credit criteria. Students must still meet the lender’s credit and eligibility requirements.

Cash bonuses are available only for certain lenders. On the rate check results on Juno you will see the cash bonus next to the offer if a cash bonus is available for that lender. The cash bonus (for the eligible lenders) is 0.5% of the loan amount.

ELFI Private Student Loan is launching a new loan for healthcare profession students called EdMed with new features tailored to your unique training path. Degrees covered include MD, DO, DDS, DMD, DPM, MSN, DNP, DVM, OD, and PharmD

Benefits:

Earnest is built to support future medical professionals with a flexible private student loan designed around the realities of medical school and residency. With competitive fixed rate APRs1 (including a 0.25% Auto Pay discount 2 ) and zero fees 3 — no origination fees, late fees, or disbursement fees — you can focus more on your education and less on extra costs.

You can cover up to 100% of your school-certified cost of attendance and benefit from features designed for the long path ahead, including a 9-month grace period 4 after graduation and up to 48 months of residency deferment.

Earnest also gives you flexibility when life happens. You can skip one payment every 12 months without penalty when eligible, 5 and choose from four repayment options 6 and flexible loan terms 7 to help find a monthly payment that fits your budget.

Checking your eligibility takes about two minutes with no impact to your credit score, and the streamlined mobile application is protected with end-to-end encryption for added peace of mind.

Plus, existing eligible Earnest clients may qualify for a 0.25% Loyalty Discount 8 , and you can reduce your rate by an additional 0.25% with Auto Pay 2.

Compare rate from top lenders. Find multiple options in just minutes. You can prequalify for offers from multiple lenders after filling out one form. Top lenders including Sallie Mae and College Ave. The $99 bonus is The White Coat Investor’s flagship course, Fire Your Financial Advisor: STUDENT for free.

Get your rate in 3 minutes. Flexible repayment options to help you find the loan that fits your budget. Applying with a cosigner may increase your chances of approval and getting a better rate. Over 1 million students have chosen SoFi.